If you haven’t opened a Roth IRA yet, do it this week. It is one of the best financial decisions you can make, and most people wait far too long to start.

What is a Roth IRA?

A Roth IRA is a type of individual retirement account with a key tax advantage: your money grows tax-free, and qualified withdrawals in retirement are also tax-free. You contribute money you’ve already paid taxes on, so you never pay taxes on the growth.

Compare that to a traditional IRA or 401(k), where you get a tax break now but pay taxes on everything when you withdraw in retirement. The Roth flips that: you pay taxes now (on a smaller amount) and never again.

Why the Roth is so powerful

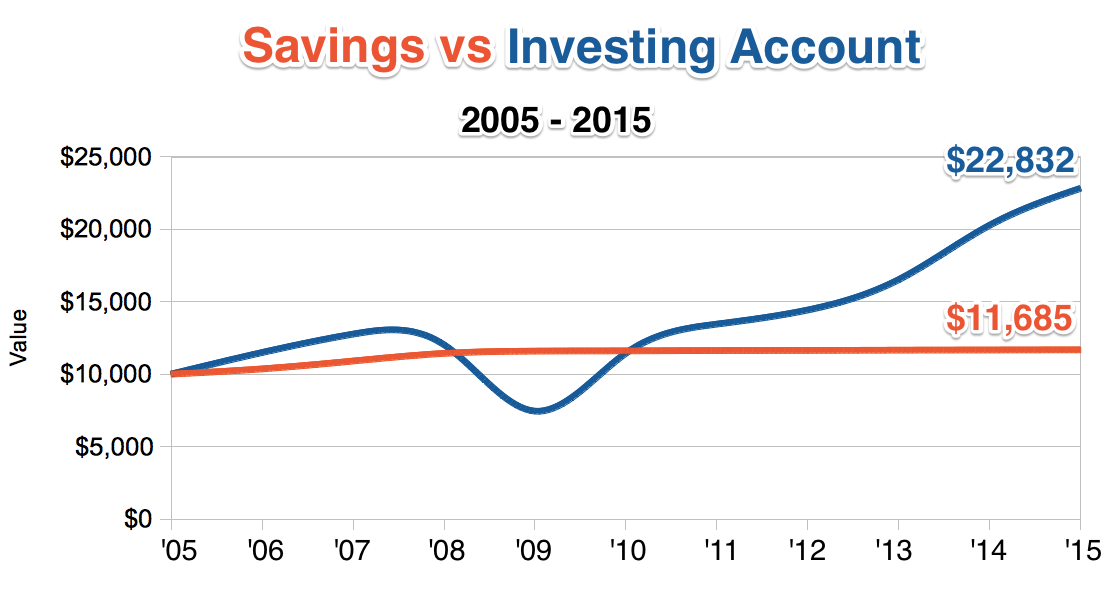

The magic is compound growth over time. When your investments grow for 20 or 30 years without being taxed, you end up with significantly more money than the same investments in a taxable account.

Here’s a simple example. If you invest $6,000 per year starting at age 25 and earn a 7% average annual return, by age 65 you’d have roughly $1.3 million. In a Roth IRA, you’d owe zero taxes on that. In a taxable account, you’d owe capital gains taxes as you withdraw.

A Roth IRA also has some useful flexibility that other retirement accounts don’t:

- You can withdraw your contributions (not the earnings) at any time, for any reason, with no penalty or taxes. This makes it useful as a backup emergency fund if needed.

- There are no required minimum distributions at age 73, unlike traditional IRAs and 401(k)s.

- You can keep contributing as long as you have earned income, with no age cutoff.

Who can contribute to a Roth IRA?

You need earned income to contribute, meaning wages, salary, or self-employment income. Investment income doesn’t count.

There are also income limits. For 2024, the ability to contribute phases out for single filers earning between $146,000 and $161,000, and for married couples filing jointly between $230,000 and $240,000. If you’re under those limits, you can contribute the full amount.

The annual contribution limit for 2024 is $7,000 if you’re under 50, and $8,000 if you’re 50 or older.

Where to open a Roth IRA

The best places to open a Roth IRA are low-cost brokerages that offer index funds:

- Fidelity is a top choice with zero-fee index funds, no account minimums, and an easy-to-use platform.

- Vanguard pioneered low-cost index investing and remains excellent for long-term investors.

- Schwab is another strong option with no minimums and competitive funds.

Avoid banks that only offer savings accounts inside the IRA wrapper. You want access to stock and bond index funds so your money can actually grow over time.

What to invest in once you open it

Keep it simple. Put your Roth IRA money into one of these:

- A total U.S. stock market index fund (like FSKAX at Fidelity or VTSAX at Vanguard)

- An S&P 500 index fund (like FXAIX at Fidelity or VFIAX at Vanguard)

- A target-date retirement fund based on your expected retirement year, if you want a single hands-off option

Pick one, set up automatic monthly contributions, and don’t check the balance obsessively. Time in the market beats timing the market.

How much should you contribute?

Max it out if you can. For most people in their 20s and 30s, this is the single best place to invest after capturing any employer 401(k) match.

If you can’t max it out, contribute whatever you can. Even $50 or $100 per month is worth starting. You can always increase it later. The important thing is to open the account and start the habit.

Open it today

The hardest part is the five minutes it takes to actually open the account. Go to Fidelity.com or Vanguard.com, click “Open an account,” and choose Roth IRA. You’ll link your bank account, transfer some money, and choose a fund. That’s it.

Every year you wait is a year of tax-free growth you don’t get back. Start now.