If you want to retire comfortably and stop worrying about money, you need a plan. Not a complicated one. A simple one you actually follow.

This is that plan.

Step 1: Earn money

You can’t build wealth without income. That might seem obvious, but a lot of people spend energy looking for shortcuts instead of focusing on earning more. Get a job. Build a skill. Get promoted. Start a side hustle. The bigger your income, the faster this plan works.

But income alone doesn’t make you wealthy. Plenty of high earners are broke. What matters is what you keep.

Step 2: Spend less than you earn

This is the entire secret to building wealth. Spend less than you earn. Everything else is just execution.

To do this, you need a budget. Not a complicated spreadsheet, just an honest look at where your money goes each month. Track your income, subtract your fixed expenses (rent, car, insurance), then figure out how much you actually have left. That gap between what you earn and what you spend is your wealth-building fuel.

If that number is zero or negative, you need to either cut spending or increase income. There’s no other option.

Step 3: Get rid of debt

Debt is the biggest obstacle between most people and financial freedom. High-interest debt, especially credit cards, destroys wealth faster than almost anything else.

Pay off all consumer debt (credit cards, car loans, personal loans) using the debt snowball or debt avalanche method. List your debts, attack them one by one, and don’t stop until they’re gone. The only possible exception is a low-interest mortgage, which some people choose to keep while investing the difference.

Step 4: Build an emergency fund

Before you invest aggressively, make sure you have 3 to 6 months of living expenses saved in a high-yield savings account. This is your financial shock absorber. When something breaks, someone gets sick, or you lose a job, you handle it with cash instead of debt.

Without an emergency fund, one bad month can undo months of progress.

Step 5: Save and invest, in this order

Once you’re debt-free (except maybe a mortgage) and have your emergency fund, invest in this order:

- 401(k) up to your employer match. This is a 50% or 100% instant return on your money. Always capture the full match first.

- Roth IRA, up to the annual limit. Your money grows tax-free. This is one of the best wealth-building tools available to most people.

- Max out your 401(k). After your Roth IRA is maxed, go back and contribute as much as possible to your 401(k).

- Taxable brokerage account. Once your tax-advantaged accounts are maxed, invest in a regular brokerage account.

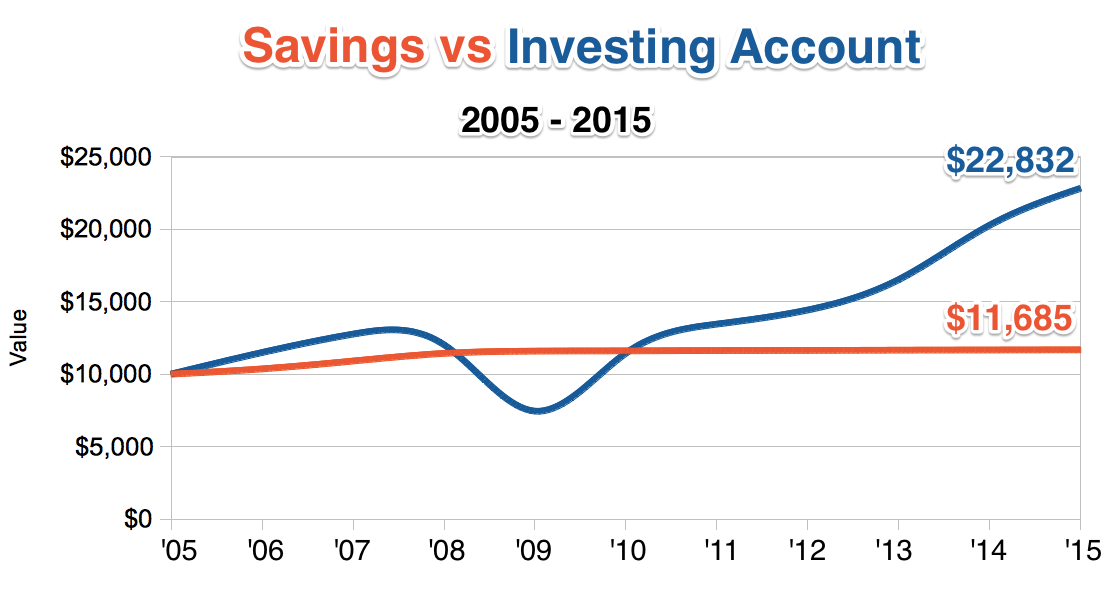

In every account, invest in low-cost index funds. The S&P 500 index and total market index funds from Fidelity, Vanguard, or Schwab are excellent choices. Don’t try to pick stocks or time the market.

Step 6: Save first, not last

The single most powerful habit in personal finance is paying yourself first. Set up automatic transfers so your savings and investments move out of your checking account on payday, before you have a chance to spend them.

When saving happens automatically, you adjust your spending to whatever is left. When saving is optional, it usually doesn’t happen.

How long does this take?

It depends on your income, your expenses, and how aggressively you save. Someone who saves 15% of their income will reach financial independence in roughly 40 years. Someone saving 30% can get there in about 25 years. At 50% savings rate, many people retire in 15 to 17 years.

The math is not complicated. The hard part is actually doing it, consistently, for years.

Start now

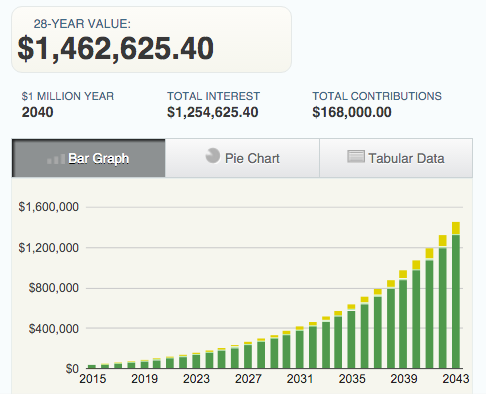

The best time to start was ten years ago. The second best time is today. Even small amounts invested consistently over decades grow into life-changing sums thanks to compound interest.

Open a Roth IRA this week if you don’t have one. Increase your 401(k) contribution by 1% this month. Cut one spending category. Do something today.

The people who retire comfortably aren’t smarter or luckier than everyone else. They just started earlier and stayed consistent.

The easy way to beat 90% of professional investors is to invest that money in low cost index funds through ETF’s. That’s it. That’s all you need to know. It took me 10 years to learn this, but when I figured it out and back tested it, I laughed at how obvious and simple it is. Then I wondered why no one was teaching this. This should be taught in middle school and retaught in high school. So I vigorously scoured the internet and sure enough, tons of intelligent, respectable advisors and financial magazines tout the benefits of index investing and how professional fund managers don’t “beat the market”. And when professional investors say don’t “beat the market”, the market = index funds. It all seems so obvious, yet for some reason it’s not. So I’m here to bring the obvious to light. It’s index funds all day long, baby. Follow this advice and you’ll be earning money like those wealthy 1% who pay less tax than you. If you can’t beat ’em, invest in them!

The easy way to beat 90% of professional investors is to invest that money in low cost index funds through ETF’s. That’s it. That’s all you need to know. It took me 10 years to learn this, but when I figured it out and back tested it, I laughed at how obvious and simple it is. Then I wondered why no one was teaching this. This should be taught in middle school and retaught in high school. So I vigorously scoured the internet and sure enough, tons of intelligent, respectable advisors and financial magazines tout the benefits of index investing and how professional fund managers don’t “beat the market”. And when professional investors say don’t “beat the market”, the market = index funds. It all seems so obvious, yet for some reason it’s not. So I’m here to bring the obvious to light. It’s index funds all day long, baby. Follow this advice and you’ll be earning money like those wealthy 1% who pay less tax than you. If you can’t beat ’em, invest in them!

A common question from readers is, “Where should I put my money?” Whether it’s an inheritance, or money saved up over time, people new to having a relatively large sum of money often aren’t sure where to invest that money. Below is an example question from a woman in her 50’s and my response of where she should put her money for retirement and beyond. Though the answer can differ, here are the 4 best places that smart people put their extra money.

A common question from readers is, “Where should I put my money?” Whether it’s an inheritance, or money saved up over time, people new to having a relatively large sum of money often aren’t sure where to invest that money. Below is an example question from a woman in her 50’s and my response of where she should put her money for retirement and beyond. Though the answer can differ, here are the 4 best places that smart people put their extra money.